Open Menu

Product

Project execution

Estimating, proposals, and contracts

Project management

Change orders

RFIs & submittals

Documents & photos

Scheduling

Time tracking

Subcontractor management

Inventory management

Daily Logs

Client portal

Custom workflows

CRM

Service work

Scheduling & dispatch

Invoicing & payments

Client communication

Field ops & asset management

Finances

AIA billing

Budgeting

Invoicing

Payment processing

Prevailing wage

Purchases & expenses

Job costing

Reporting & insights

Fleet tracking

Integrations

Trades

Trade contractors

Electrical

Plumbing

HVAC

Painting

Remodeling

Concrete

Excavating

All other trades

Resources

The Cost Codes Show

Resources

Case Studies

Latest Resource

Business Management

How to estimate commercial HVAC jobs using historical labor data

View all resources

QuickBooks

Accounting

QuickBooks Online

Intuit Enterprise Suite

QuickBooks Desktop

Other QuickBooks Integrations

QuickBooks Online Payroll

QuickBooks Payments

QuickBooks Time

Pricing

Training & support

What to expect with Knowify

Become a certified advisor

Customer support center

Login

Request a Demo

Resource center

Learn with Knowify

Select Topic

All Topics

Business Management

Construction bookkeeping & accounting

Construction industry news

Construction project management & execution

Construction team management

Customer story

Knowify product updates

The Cost Codes Show

Select Type

All Types

Accounting

Article

Knowify training webinars

Podcast

Product Overview

Clear

Business Management

How to estimate commercial HVAC jobs using historical labor data

Construction bookkeeping & accounting

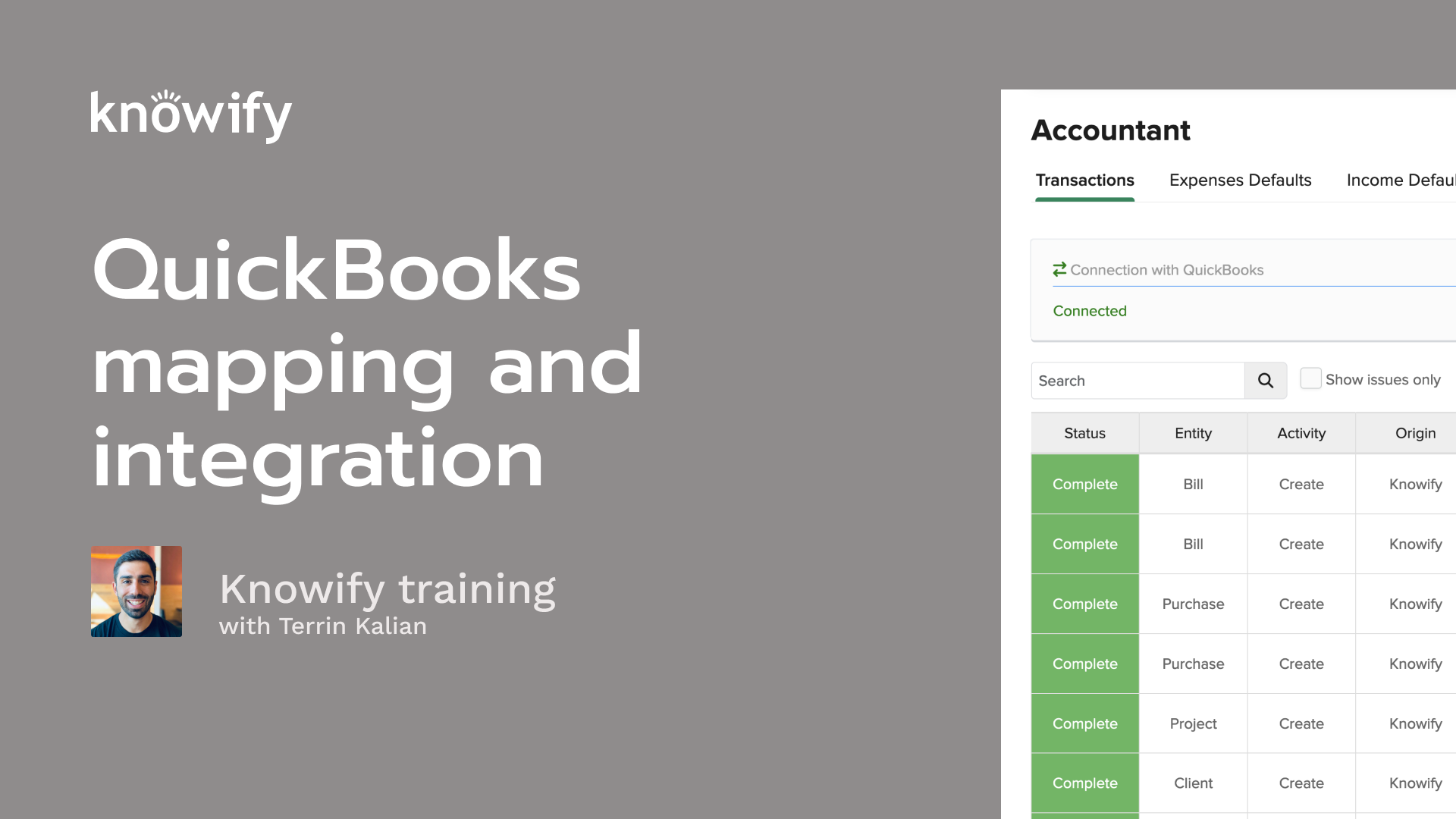

QuickBooks mapping and integration

Business Management

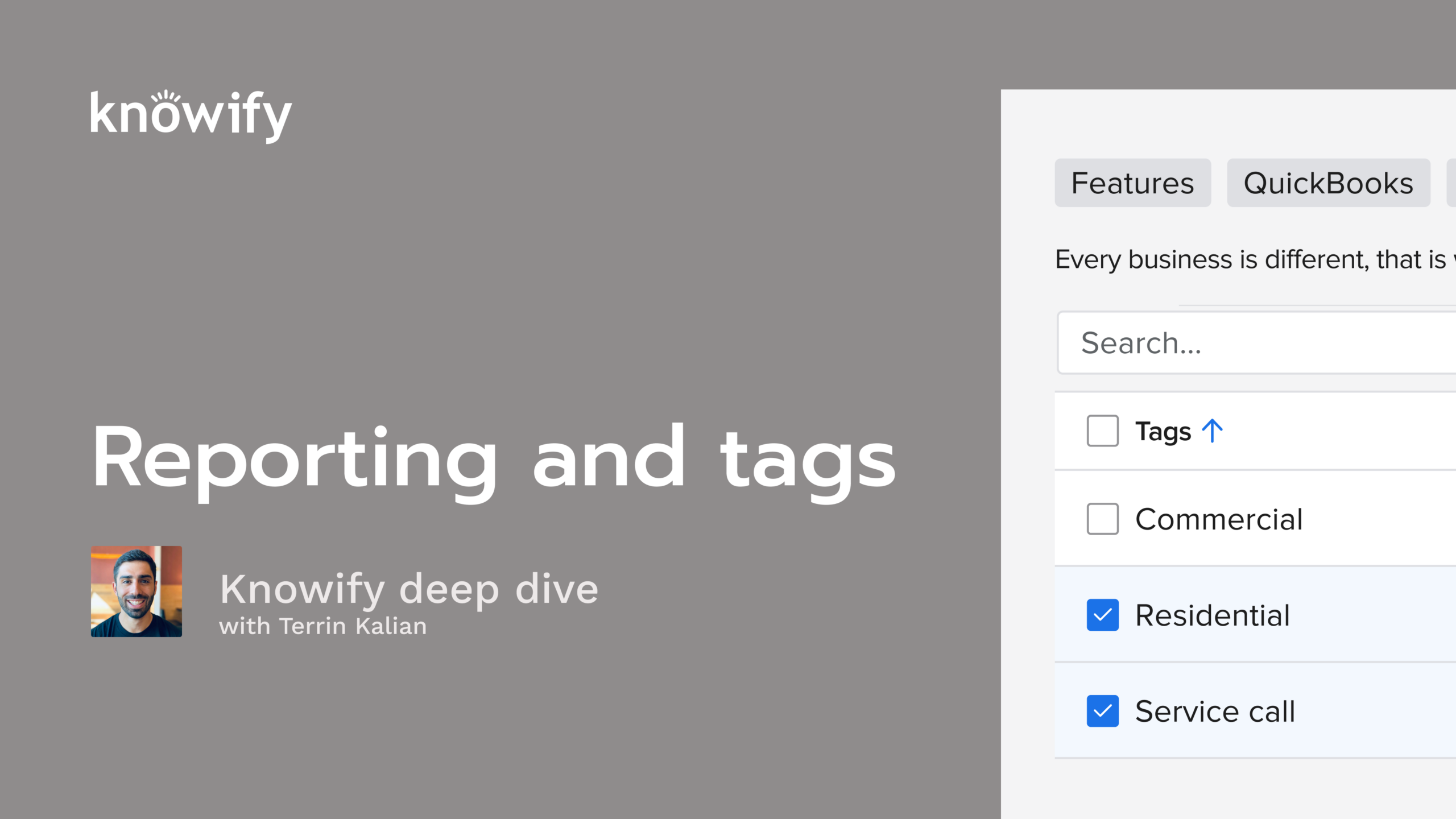

Knowify deep dive: Reporting and tags

Construction project management & execution

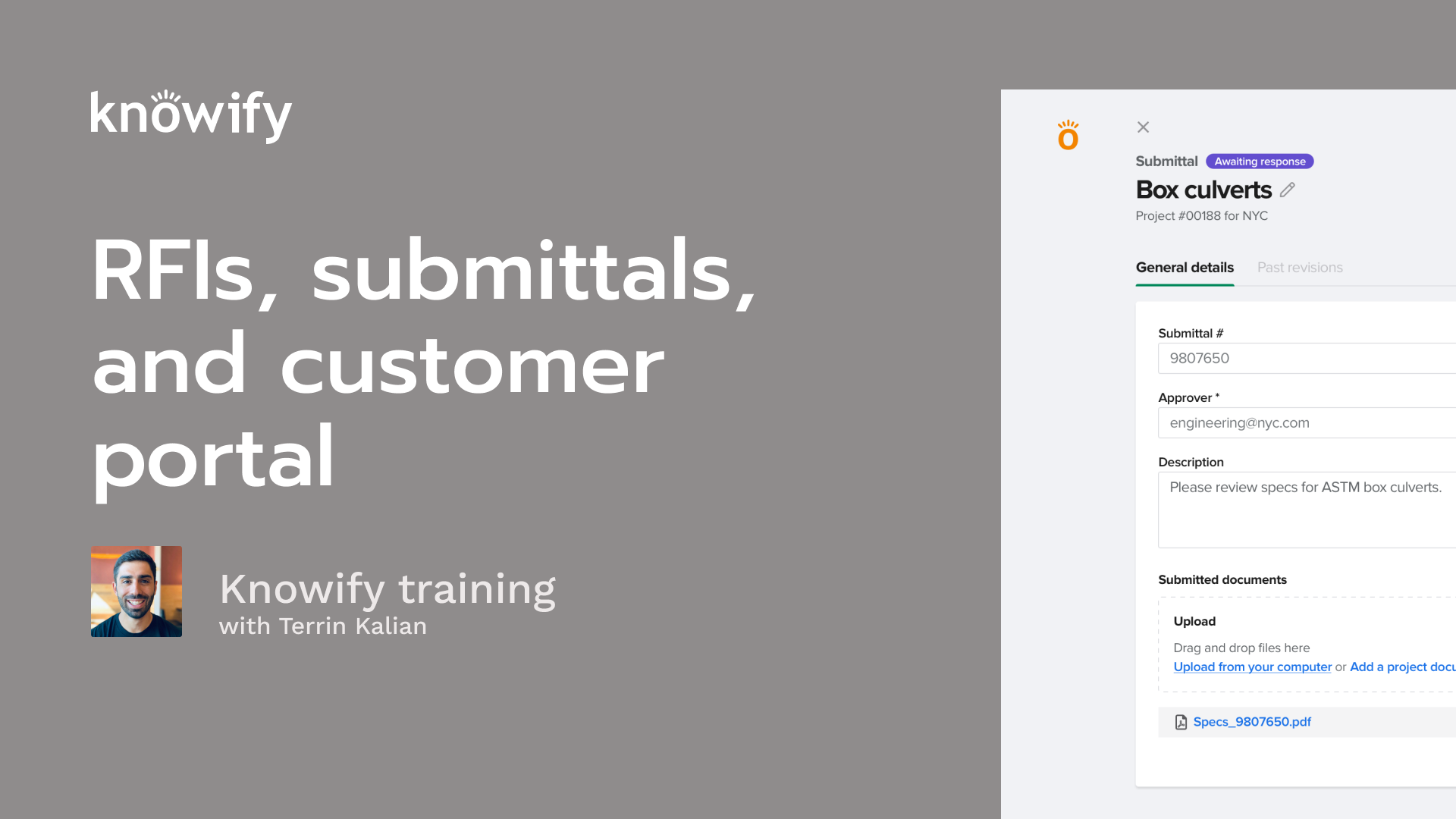

Client and project communication: RFIs, submittals, and the customer portal

Business Management

The ultimate guide to building a QuickBooks-centered construction tech stack

Construction team management

Mentorship and learning in construction: Why staying curious matters for your career

Business Management

Construction tech: What works for subcontractors and what doesn’t

Construction project management & execution

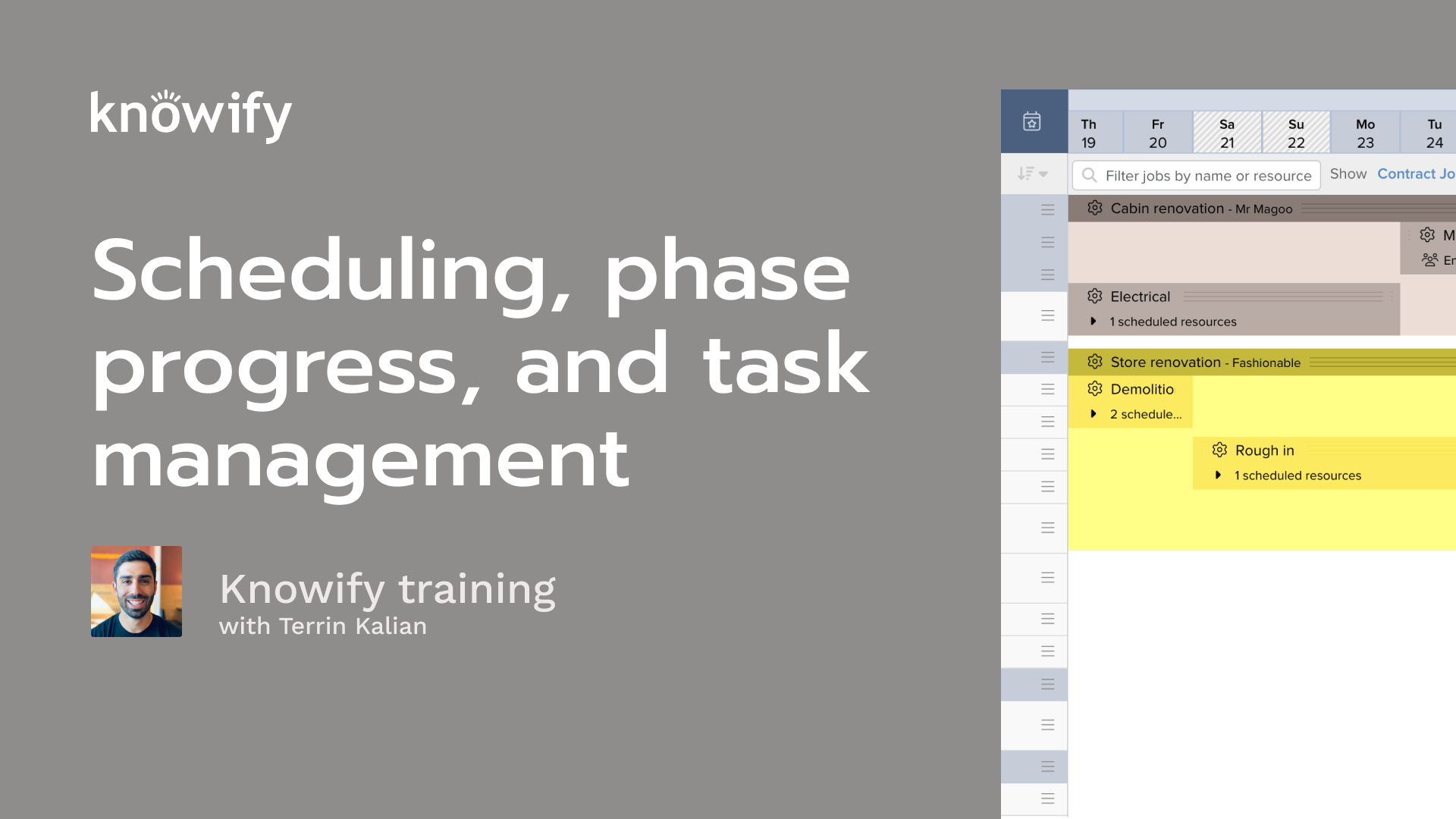

Scheduling, phase progress, and task management

Business Management

When should subcontractors invest in construction management software?

Business Management

Pricing with confidence: How contractors can win more profitable work

Construction project management & execution

From the field: Lessons learned in construction project management

Business Management

Growth milestones: How subcontractors can scale from solo operations to structured teams

1

2

3

…

26

Next